Agents

are our

Priority

®

Alliant National is on a mission to empower independent title agents while protecting

property owners with secure title insurance.

property owners with secure title insurance.

We’re On Your Side

Alliant National has no direct operations to compete against independent agents like the big underwriters, so we can dedicate all our resources to helping independent agents thrive.

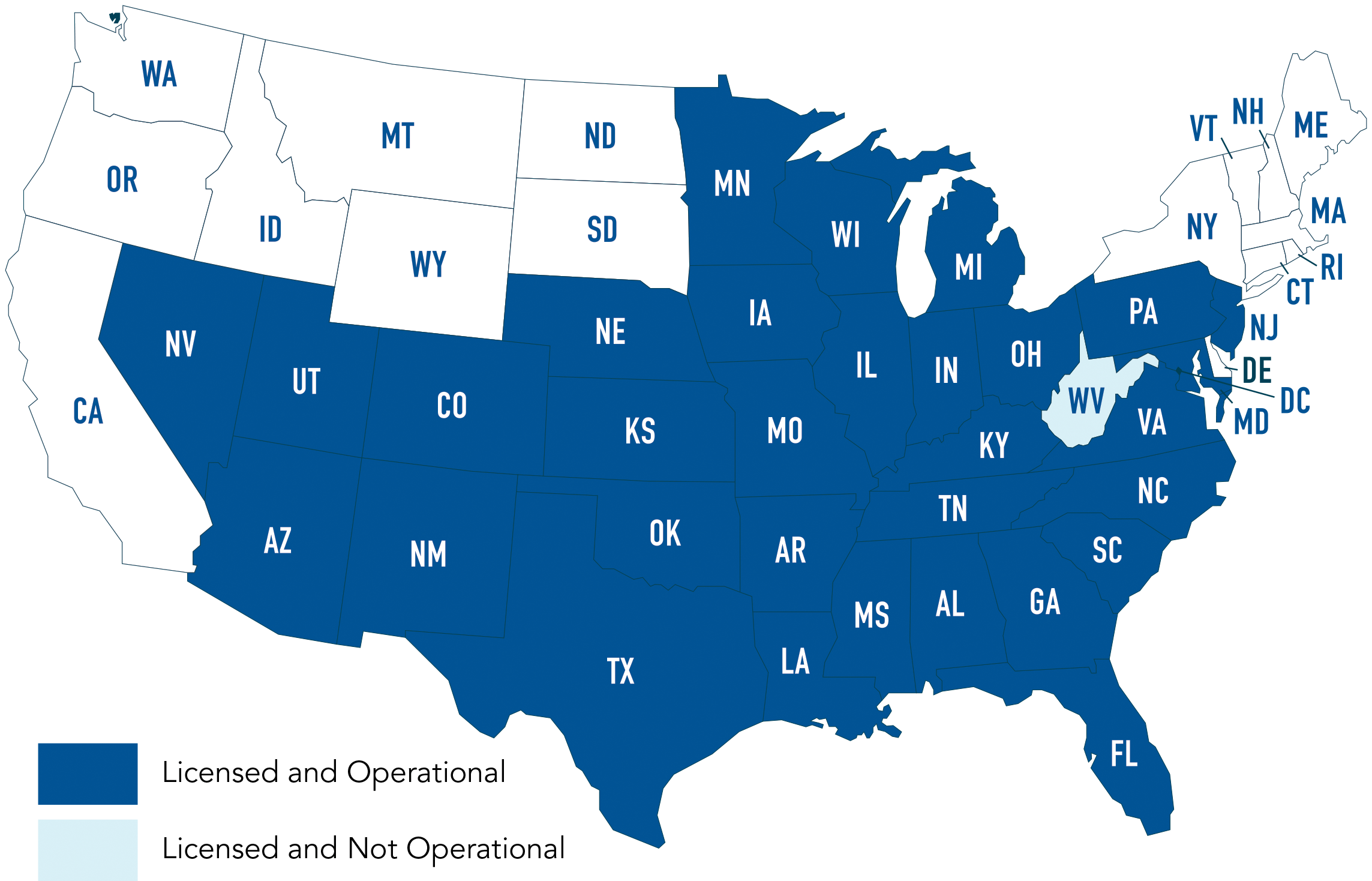

Where We Operate

Founded in 2005 and growing with a seasoned group of title insurance professionals, business leaders, and entrepreneurs, Alliant National serves thousands of title professionals as a licensed underwriter in 32 states and Washington, D.C., with corporate headquarters at the foot of the Rocky Mountains in Longmont, Colorado. Alliant National is proud to be a part of the Dream Finders Homes family.

| The Alliant National Way

Put people at the center of the relationship

Every independent agent aspires to be a partner

with Alliant National

Empower independent agents while protecting property owners with secure title insurance

Caring

3Cs: Culture of Trust

Alliant National nurtures a Culture of Trust. Being trustworthy requires our team members to practice the 3Cs.

1. Competence we continue to develop our competence - pursue mastery, share our knowledge and continue to learn;

2. Caring we demonstrate care for others by being genuine, patient and uncommonly helpful;

3. Commitment we keep our commitments by setting expectations, doing what we say, and accepting unconditional responsibility for the outcomes we produce.