Join Our Team at Alliant National Title Insurance Company

At Alliant National, we pride ourselves on being more than just a title insurance company-we're a collaborative, people-first organization that values integrity, innovation, and meaningful relationships. Our team is passionate about delivering outstanding service while fostering a culture built on respect, trust, and teamwork.

Great Place to Work and Fortune Best Small Workplace and Best Place to Work in Real Estate

Great Place to Work® (GPTW) is the global authority on high-trust, high-performance workplace cultures. Over 10 million employees in 50 countries annually take the Trust Index© Employee Survey, its proprietary research tool.

One of our strategic objectives is to become the best place to work in our industry. The annual GPTW Trust Index survey provides us with independent feedback to measure our progress and identify gaps in supporting our people.

In 2025, 98% of our employees affirmed that Alliant National is a great place to work. Visit our page on Great Place to Work®.

Employee Benefits Include:

- Medical, Dental, and Vision Insurance

- 401(k) Retirement Plan with employer contributions

- Flexible Spending Account (FSA) and Health Savings Account (HSA)

- Life and Disability Insurance

- Competitive Paid Time Off (PTO)

- 11 Paid Holidays

- A culture that encourages growth, flexibility, and community impact

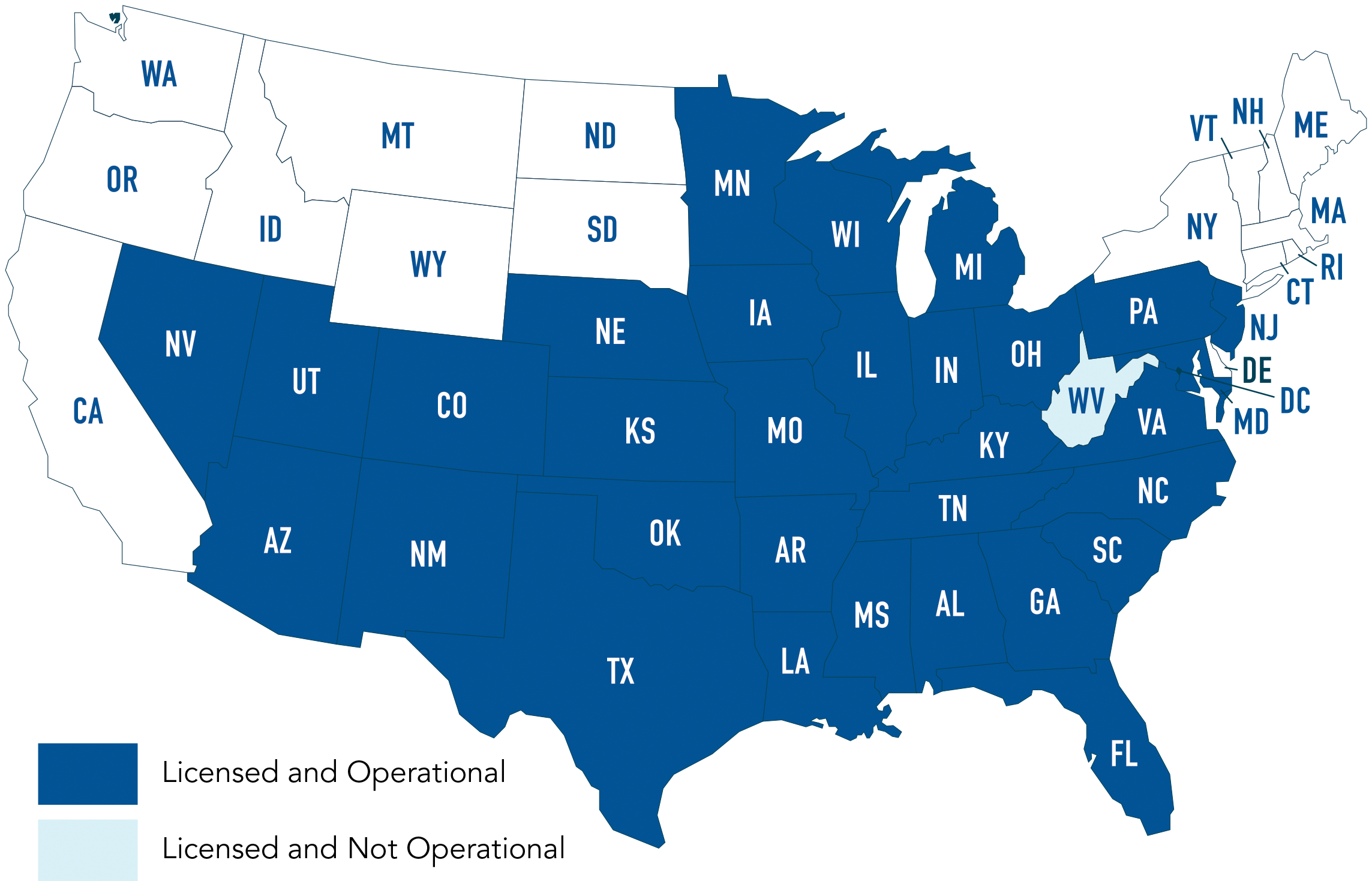

No matter where you are, you have a place to work here

We have a staff of dedicated professionals with diverse skill sets and backgrounds who share a desire to help people and businesses thrive.

Our teams live and work across the country. No matter where you are you have a place here. Work from home options are often available, and we are passionate about promoting a work/life balance.